The Impact of Taking Social Security at 62, 65, 67, or 70

One of the biggest decisions you’ll make in retirement is when to start taking Social Security. Your monthly benefit amount depends on when you claim it, and choosing the right time can have a major impact on your long-term financial security. This guide breaks down what happens when you claim at 62, 65, 67, or 70, helping you make the best decision for your situation.

FINANCIAL FREEDOM/ RETIREMENT PLANNING60 AND BEYOND

Tonia Perry

2/27/20254 min read

One of the biggest decisions you’ll make in retirement is when to start taking Social Security. Your monthly benefit amount depends on when you claim it, and choosing the right time can have a major impact on your long-term financial security.

This guide breaks down what happens when you claim at 62, 65, 67, or 70, helping you make the best decision for your situation.

How Social Security Benefits Are Calculated

Your Social Security check is based on:

✔️ Your 35 highest-earning years

✔️ Your full retirement age (FRA) – This is the age when you can collect 100% of your benefits

✔️ When you start claiming – Benefits decrease if you claim early and increase if you wait past FRA

📌 Your Full Retirement Age (FRA) Depends on Your Birth Year:

Born 1943-1954 → FRA is 66

Born 1955-1959 → FRA gradually increases (e.g., 66 and 2 months for 1955, 66 and 4 months for 1956, etc.)

Born 1960 or later → FRA is 67

Now, let’s compare how claiming at different ages affects your monthly benefit.

Taking Social Security at Age 62: The Early Option

Pros:

✅ Start receiving money sooner

✅ Helpful if you need income now

✅ Can work part-time while receiving benefits

Cons:

🚨 Permanent benefit reduction – You’ll get about 25-30% less per month for life

🚨 Earnings limit applies – If you work while collecting before FRA, your benefits may be temporarily reduced

💡 Best for: Those who need income immediately, have health concerns, or don’t expect to live into their 80s or beyond.

Taking Social Security at Age 65: The Midpoint

Pros:

✅ Smaller reduction than claiming at 62

✅ You qualify for Medicare at 65, making healthcare planning easier

✅ Good option if you retire early but want to reduce your penalty

Cons:

🚨 Still not full benefits – Monthly checks will be 7-13% lower than if you waited until FRA

🚨 If you continue working, benefits may still be subject to the earnings limit

💡 Best for: Those who retire early but want a higher benefit than at 62.

Taking Social Security at Age 67: Full Retirement Age (FRA)

Pros:

✅ Receive 100% of your earned benefit

✅ No penalties or reductions

✅ No earnings limit – You can work and collect benefits without reductions

Cons:

🚨 You miss out on 5 years of early payments (compared to claiming at 62)

💡 Best for: Those who can afford to wait and want to maximize benefits without delaying too long.

Taking Social Security at Age 70: The Maximum Benefit

Pros:

✅ Highest possible monthly payment – Benefits grow 8% per year after FRA until 70

✅ No earnings limit – You can work as much as you want without penalty

✅ Ideal for those who live longer and want to maximize retirement income

Cons:

🚨 You must delay benefits for several years

🚨 Requires other income sources until you start collecting

💡 Best for: Those in good health who want the highest lifetime payout and can afford to wait.

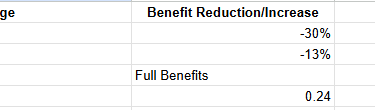

Comparing Monthly Benefits by Age

Let’s say your full retirement benefit at FRA (67) is $2,000 per month. Here’s what you’d receive at different claiming ages:

Claiming AgeBenefit Reduction/IncreaseMonthly Benefit62-30%$1,40065-13%$1,74067 (FRA)Full Benefits$2,00070+24%$2,480

If you claim at 62, you get less per month, but if you wait until 70, you receive a much larger check.

Lifetime Benefit Considerations

Many retirees wonder: Will I get more money overall if I take Social Security early or wait?

📌 Break-even point:

If you claim at 62, you get more checks but at a lower amount.

If you wait until 70, you get fewer checks but at a higher amount.

Most break-even points happen around age 78-80. If you live past this, delaying often results in higher lifetime earnings.

💡 Health and life expectancy matter:

If you have health concerns, taking it early may make sense.

If you expect to live into your 80s or beyond, delaying could be the better financial move.

Should You Work While Collecting Social Security?

If you claim before FRA and continue working, your benefits may be temporarily reduced:

In 2024, if you earn more than $22,320 before FRA, Social Security deducts $1 for every $2 earned over the limit.

Once you reach FRA, the earnings limit disappears, and your benefit amount is adjusted to return withheld funds.

💡 Key takeaway: If you plan to keep working, delaying benefits until FRA or later can prevent temporary reductions.

Final Thoughts: What’s the Best Age to Claim?

There is no one-size-fits-all answer—it depends on your health, financial situation, and personal goals.

✅ Consider claiming early (62-65) if:

You need income immediately to cover expenses.

You have health issues and don’t expect to live long.

You have few other income sources in retirement.

✅ Consider waiting until FRA (67) if:

You want to avoid penalties and earn your full benefit.

You plan to keep working without reductions.

You want a stable retirement income without the wait.

✅ Consider delaying until 70 if:

You want the highest possible benefit.

You have other income sources to cover expenses.

You expect to live into your 80s or beyond.

No matter when you decide to start Social Security, it’s important to have a retirement income plan that balances your savings, investments, and lifestyle goals.

Need Help Planning Your Social Security Strategy?

Choosing when to claim Social Security is a big decision. I can help you navigate your options and find the best path to financial freedom in retirement.

📞 Call/Text: 216-800-7303

📧 Email: Strive.tonia@gmail.com

It’s never too late to embrace financial freedom—let’s build your retirement plan together!

EMAIL: Strive.tonia@gmail.com

PHONE:(216)800-7303

© 2025. All rights reserved.

We do not offer every plan available in your area. Currently, we represent 9 organizations which offer 80 products in your area. Please contact Medicare.gov, 1-800-MEDICARE, or your local State Health Insurance Assistance Program (SHIP) to get information on all of your options. This is a proprietary website and is not associated, endorsed or authorized by the Social Security Administration, the Department of Health and Human Services or the Center for Medicare and Medicaid Services. This site contains decision-support content and information about Medicare, services related to Medicare and services for people with Medicare. If you would like to find more information about the Medicare program please visit the Official U.S. Government Site for People with Medicare located at http://www.medicare.gov

Independent Insurance Agent | Final Expense Insurance Ohio | Medicare Advantage Plans Cleveland | Life Insurance for Children | Medigap Plans PA | Insurance Advisor for Seniors | Community Insurance Help